The PTC

4

min read

Published on

May 14, 2026

May 14, 2026

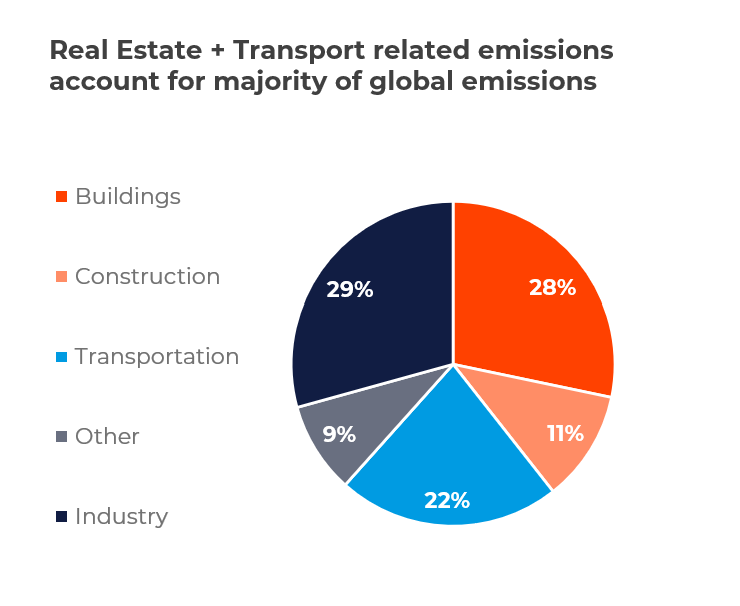

ESG has been a key focus for businesses over the past decade, with decarbonization being a key component of the environmental pillar. As real estate inherently pertains to the built environment, the industry has a large role in dictating the global carbon impacts. Historically, real estate has not been very environmentally friendly; in fact, the UN’s Environmental Program states that the industry accounts for roughly 37% to 40% of global energy-related carbon emissions.

As a result, real estate has been facing pressures to improve carbon emissions and reduce its toll on the natural environment. From demand-driven market pressure to government mandates and incentives, the industry is being driven to provide impactful solutions. For example, in New York City, under Local Law 97, buildings that exceed their annual emissions limits now face fines of $268 per metric ton of CO2 equivalent. Furthermore, investors are demanding higher standards and greater ESG certification compliance to both meet market demand and comply with their own investment mandates. The initial efforts focused on reducing the impact through energy-efficient buildings and clean material choices. However, now leaders in the space are exploring how they can reverse the impact by pulling carbon from the air and storing it indefinitely.

As the industry rushes to adapt to these new pressures, a common mistake is conflating all Carbon Capture and Storage (CCS) methods. Treating these technologies as a single solution ignores their drastically different operational requirements and outcomes.

For the purpose of this newsletter, we will be focusing on Direct Air Capture (DAC) as it is the most applicable to conventional real estate in terms of scale and requirements.

The physical and economic realities of capturing carbon are not as attractive or feasible as initially expected by climate model forecasts. Pulling carbon from the ambient air via DAC is challenging with efforts constrained by thermodynamics. To remove just one tonne of CO2, a DAC plant must process approximately 1.8 million cubic meters of air, assuming a highly optimistic 75% capture efficiency.

Furthermore, DAC economics are often misrepresented. While the industry loves to cite projected future costs of $100 to $300 per tonne, independent researchers suggest the actual, current costs are far more likely to fall between $230 and $540 per tonne.

By comparison, point-source CCS captures CO2 directly at the source (industrial sites), where the gas concentration is substantially higher. Because DAC is forced to filter diluted ambient air, it requires four to six times the energy consumption of point-source capture, raising valid questions about the grid strain it creates.

When it comes to Direct Air Capture (DAC), there are numerous approaches that vary in scale. The most conventional approach is large-scale industrial systems that employ hundreds of large fans; however, there have been examples of exploration into integrating smaller systems into building HVAC. The disparity between large industrial sites and localised pilot programs highlights the nascency of the technology.

Case study: HVAC Integrated DAC

Academic Pilot, Linköping, Sweden

The Pilot involved retrofitting existing commercial building ventilation to capture CO2 from incoming/recirculated air. Essentially, turning existing real estate (in this case a gym) into carbon capture systems while improving indoor air quality.

The project showed how this type of system could reduce the energy penalty of capture by piggybacking on existing HVAC fan airflow; however, the extremely low capture volume per unit (50–80 kg/day).

Case study: Utility-Scale DAC

An industrial-scale facility in Texas paired with deep geological sequestration networks designed to capture 500,000 tonnes of CO2 annually, the sort of scale required to make an impact on global emissions targets.

However, these systems require billions in upfront CAPEX and enormous, dedicated zero-carbon power loads just to operate the fans and heating cycles without emitting more carbon than it captures.

As Stratos is a joint venture between BlackRock and Occidental Petroleum, critics have also argued that this technology is greenwashing by oil companies to continue extracting fossil fuels while appearing environmentally responsible.

While large projects require massive capital and energy reserves, micro-deployments like the Swedish pilot offer a potential approach for conventional real estate but ultimately struggle to move the needle on meaningful global emissions reductions.

Pre-defined logic-based workflows

For the real estate sector, the most realistic and scalable way to act as carbon storage isn't through expensive and energy-intensive mechanical vacuums; it is through the building materials themselves.

Traditional construction has notoriously negatively impacted the environment; traditional cement alone accounts for roughly 8% of all global CO2 emissions. However, shifting to bio-based materials turns buildings into passive carbon vaults. Hempcrete masonry blocks can achieve a negative carbon footprint of −20.3168 kg CO2 equivalent per unit, actively locking away more carbon than is emitted during their production. When coupled with mass timber, bamboo, and other emerging bio-brick technologies, the physical structure of a building can be leveraged as a low-tech carbon sink.

In conclusion, mechanical CCS is currently only feasible at a large, centralised, industrial scale. For real estate developers and asset managers, integrating passive storage and relying on proven methods of prevention are far more realistic options.

The data strongly supports prioritising efficiency and visibility first:

With government mandates and market demand driving strategy over pure altruism, property owners have more economical alternatives to offset their footprints than mechanical capture. The true new frontier for real estate decarbonisation lies in tackling embodied carbon, tracking material supply chains, and constructing energy-efficient buildings.

.webp)

.jpeg)

.jpg)

.jpg)

.jpg)

.webp)

.jpg)

.jpeg)

.png)

.png)

.jpg)

.jpeg)

.jpeg)

.jpeg)

.jpg)

.jpg)

.png)

.jpg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpg)

.jpeg)

.jpg)

.png)

.jpeg)

.jpg)

.jpeg)

.png)

.jpg)

.png)

.png)

.png)

.jpg)

.jpg)

.jpg)

.png)

.webp)

.png)

.jpg)

.jpg)

.jpg)

.jpg)

.jpg)

.png)

.png)

.jpeg)

.png)

.jpg)

.jpeg)

.jpeg)

.png)

.png)

.png)

.jpeg)

.jpeg)

.png)