The PTC

5

min read

Published on

May 27, 2026

March 12, 2026

The investment landscape has undergone a fundamental shift where the era of easy liquidity has passed, and new funding dynamics have emerged. While capital is still available, the optionality and fit for sources of capital are changing to reflect company dynamics.

There has been a move from traditional generalist venture capital routes towards more technology and sector-specific pathways with different mixes of actors. These new investor types are filling the gap in demand that traditional venture capital can’t meet, resulting in new funding dynamics and requiring companies to adopt differing approaches to positioning for a raise.

As traditional generalist venture capital funds and other institutional capital tighten budgets, family offices and strategics are increasingly engaging with early-stage ventures. Family offices and other forms of private capital are not satisfied with recent results from some of their investments in GPs or have more confidence to invest directly. Consequently, these firms are starting to diversify away from a limited partner-only model in the venture space.

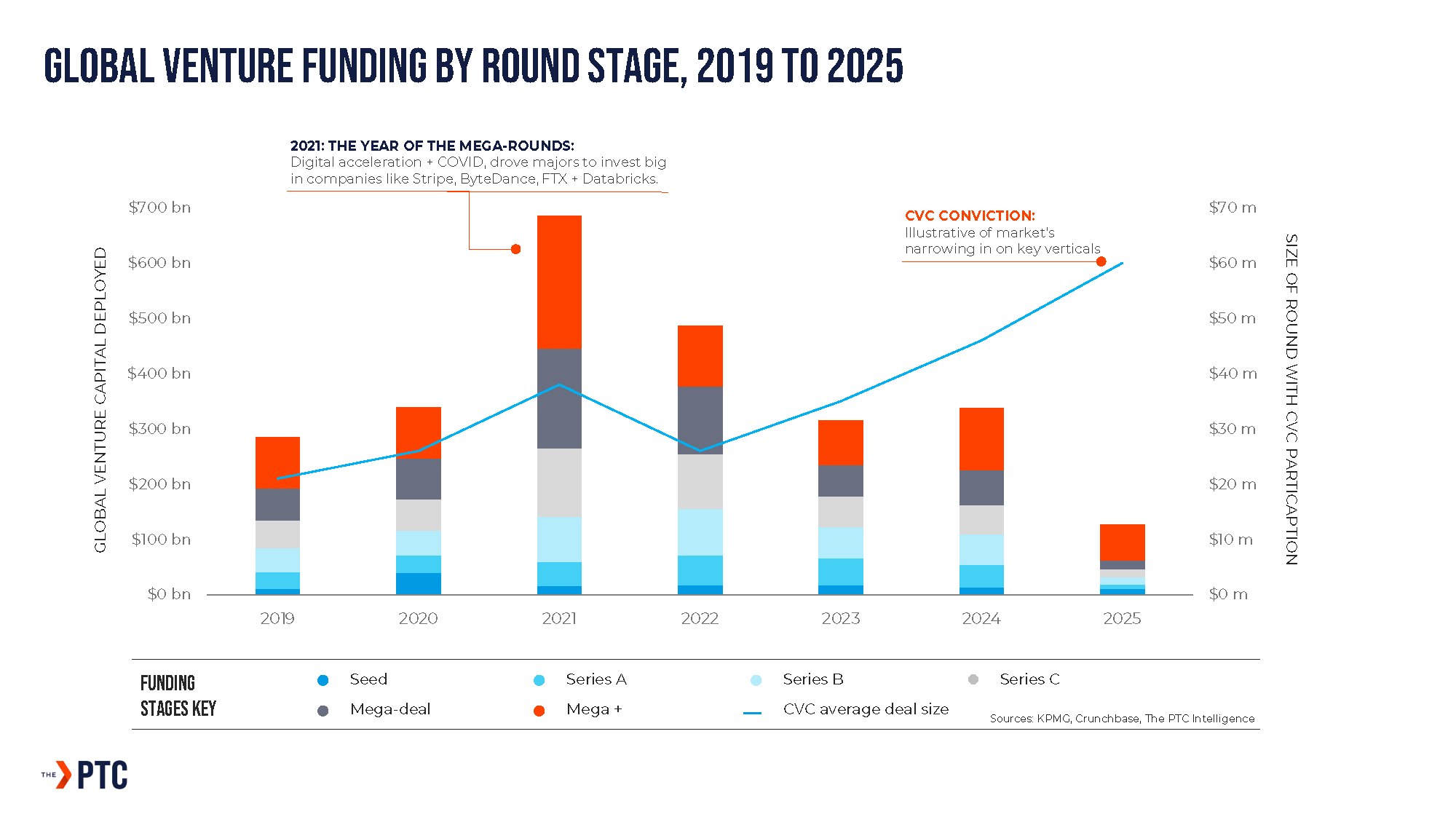

Family offices have become the largest cohort of active private capital investors by number, representing over 40% of active private capital investors. Meanwhile, CVC participation has been growing steadily over the past few years (see chart above), reflecting a broader market trend around narrowing thesis focus and deployment in key verticals.

With later stages increasingly receiving a greater share of total funding, the overlap in different investor types increases, shaping into an era of “fund ubiquity”.

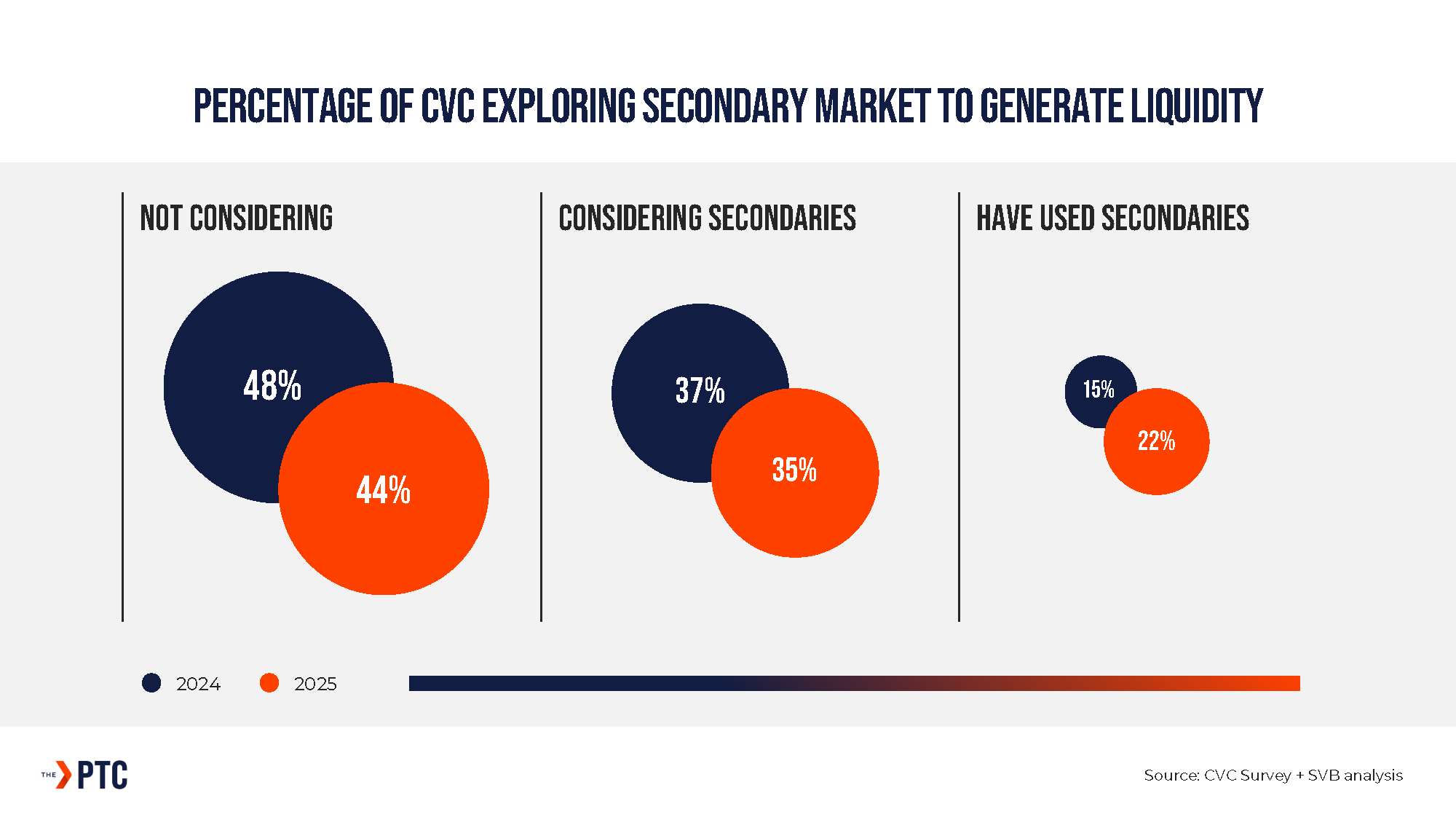

The ongoing lack of IPOs is pushing secondary market strategies and growth. Investors are looking for alternative ways to generate returns without relying on public listings.

This has led to a significant increase in secondary market activity. In 2025, we saw that 22% of corporate venture capitals (CVCs) reported using the secondary market to generate liquidity. This figure represents a 7-percentage point increase from the previous year, highlighting how these investors are actively managing their portfolios in the absence of exits that would traditionally have been available.

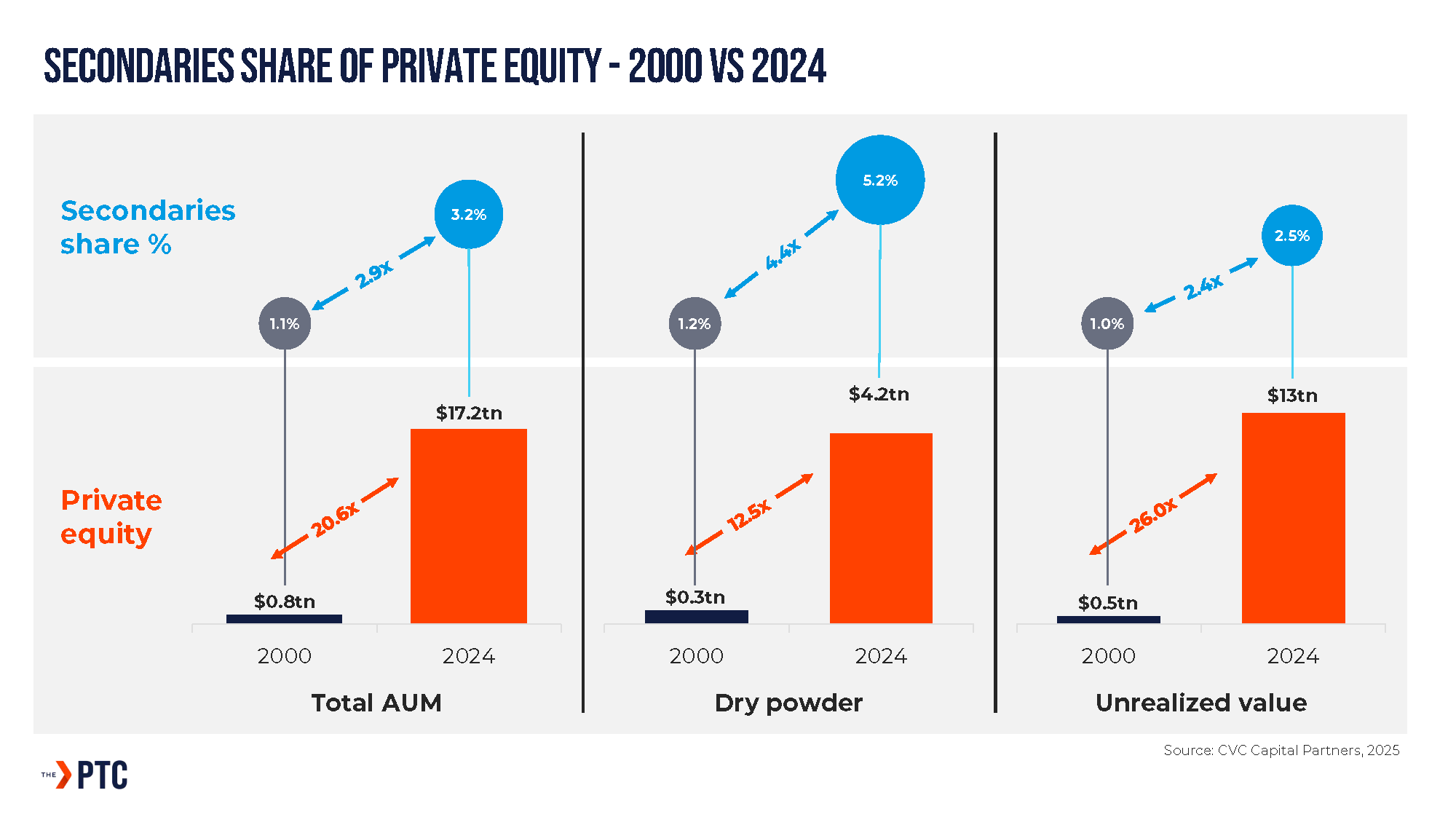

As a result, global secondary market volumes have also hit record highs. Jefferies secondary market analysis reveals that volumes reached approximately $103bn in the first half of 2025 alone, a 51% uplift from H12024. This data suggests that secondaries are no longer just an option during strained conditions but a core tool for liquidity.

These changes have resulted in significant shifts to the capital environment. We saw a recovery in capital invested during 2025, but the nature of that capital is more concentrated due to investors bringing burnt post 2021.

Funding is flowing primarily into larger deals and concentrated themes linked to the AI space (e.g. data centres, energy). Recent funding data tell a clear story of consolidation towards later-stage ventures. CRETI analysis of transaction data revealed that of the $16.7 billion invested during the year, we saw $12 billion allocated to funding of $100 million or more. There has also been a noticeable shift towards more focused investment thesis amongst funds, executing deals in areas that align most with core expertise.

Just 35 companies accounted for 72% of total capital invested, reflecting a trend that is creating a challenging environment for smaller players. The market is clearly favouring established and proven players in familiar or hot industries, rather than spreading bets across the broader ecosystem.

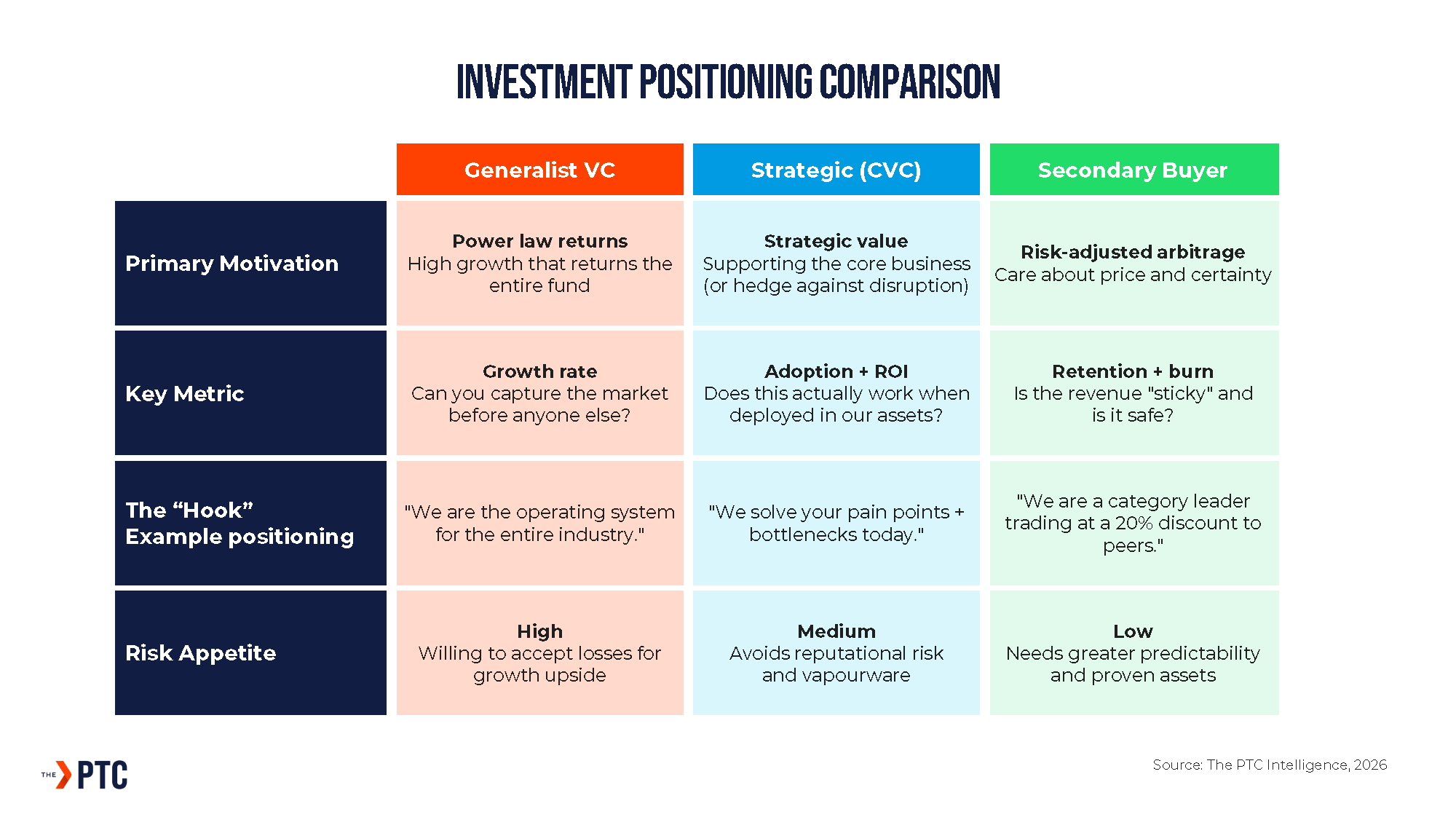

These new investment dynamics and increasing interest from non-VCs have real implications for companies looking to raise funds for strategic or operational reasons. Differing motivations across a diverse group of proptech investors mean that understanding the nuances in motivation is critical for teams constructing boards, cap table and funding strategy.

Because motivations differ, the narrative and metrics hit in the pitch must also differ. A pitch to a strategic investor needs to highlight different KPIs than a pitch to a generalist VC, which is also a different positioning for the secondary buyer, etc.

Generalist VCs are looking for high growth in a few of their investments to return for the entire fund and therefore look to key metrics around growth. Strategic investors such as CVCs place more emphasis on adoption and ROI metrics, looking to see if there is proven realisable value that could benefit capabilities. Meanwhile, positioning for the secondary market requires considerations beyond narrative and KPIs, facilitating the option through business strategy. Secondaries typically have a lower risk appetite and are looking to trade on more predictable assets.

The table below reveals a key summary of the types of considerations key to understanding shaping positioning for investment.

We are experiencing a two-paced environment with a clear separation between exploratory ventures and assets with proven value realisation (later stage) or high-demand fields like those AI-related, which accounted for 58% of combined venture deal value in 2025.

The resulting shift in the investment landscape has driven differences in growth timelines across the ecosystem. Successful companies in this cycle will be those who can navigate these shifts and must align themselves with the right capital strategy and partner for their specific stage and sector.

.webp)

.jpeg)

.jpg)

.jpg)

.jpg)

.webp)

.jpg)

.jpeg)

.png)

.png)

.jpg)

.jpeg)

.jpeg)

.jpeg)

.jpg)

.jpg)

.png)

.jpg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpg)

.jpeg)

.jpg)

.png)

.jpeg)

.jpg)

.jpeg)

.png)

.jpg)

.png)

.png)

.png)

.jpg)

.jpg)

.jpg)

.png)

.webp)

.png)

.jpg)

.jpg)

.jpg)

.jpg)

.png)

.jpg)

.jpeg)

.jpeg)

.png)

.png)

.png)

.jpeg)

.jpeg)

.png)