The PTC

3

min read

Published on

May 27, 2026

April 30, 2026

Construction technology (Contech) has long been identified as a laggard compared to the impact technology has had on adjacent sectors like manufacturing. The level of innovation has been subdued largely due to the siloed nature of the construction ecosystem, which has made achieving sufficient scale and traction without a coordinated technology strategy challenging.

We have seen increased interest from our clients in the construction space in using technology to bring value across the construction lifecycle, as the structural challenges have remained stubbornly present. This interest has crystallised and accelerated M&A activity in a range of tech solutions covering both software platforms and hardware, impacting physical construction and supply chains.

The obvious strategy being pursued is controlling and then streamlining across the construction value chain, but there are different approaches being taken depending on the role within the ecosystem.

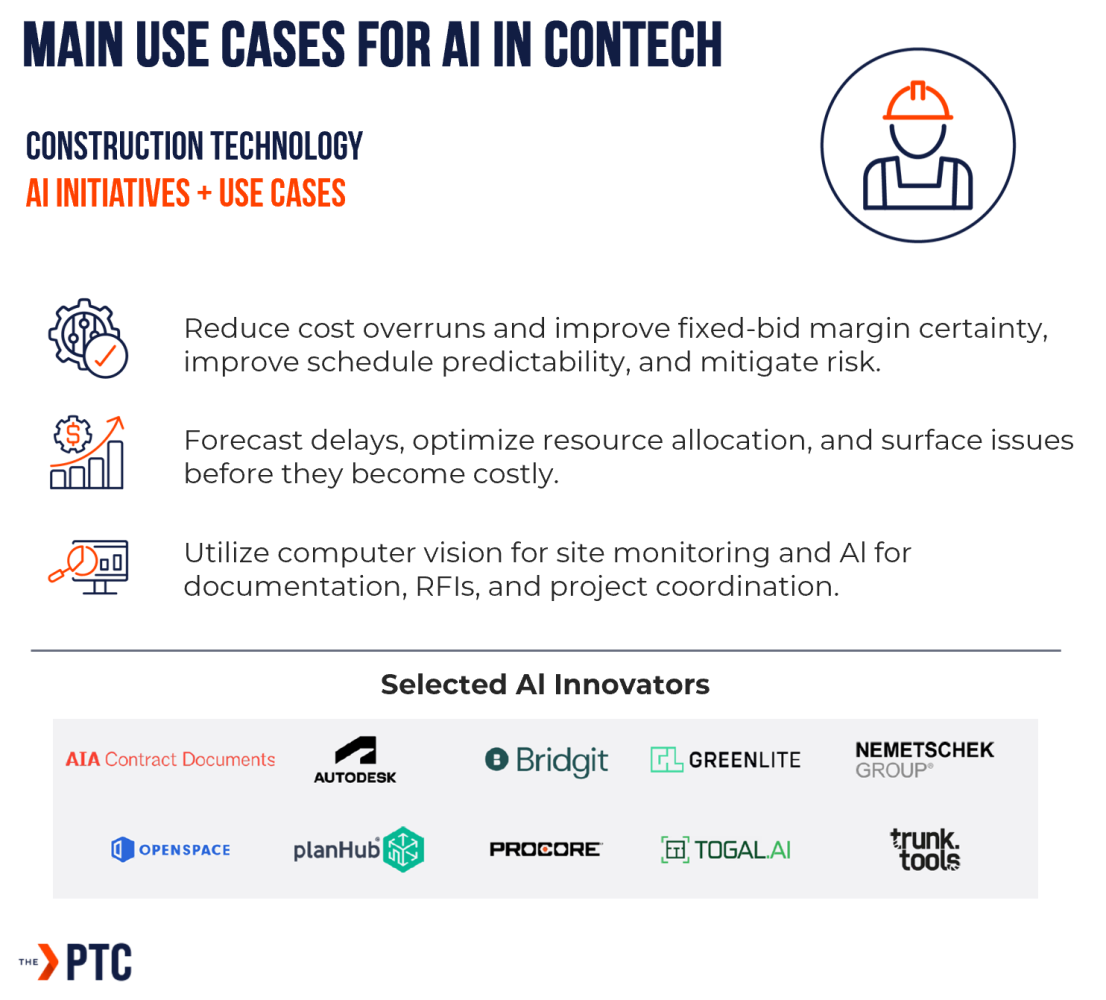

The main success stories in Contech have been, to date, point solutions. Project management tools, scheduling and contracting software or data dashboards with some of the standout names in proptech/ contech emerging in this space, including Procore, etc.

Whilst often great solutions, the impact on the overall project or portfolio has been reduced due to:

·Incomplete usage across different actors

·Limited digital maturity on job sites

· A lack of end-to-end system workflows

We have seen technology evolve and start to work across the construction lifecycle. Initially, this was driven by software layers and integrations with core systems (such as Autodesk and peers) acting as an anchor for other use cases / processes.

This has now transitioned into consolidation of platforms and business models where capabilities are expected across the entire construction flow from planning to on-site build to handover to building management.

This reflects the realisation in the industry that the complexity and inefficiency in construction (with the squeezed margins) could not be addressed without connecting the tools together in a coherent, structured way.

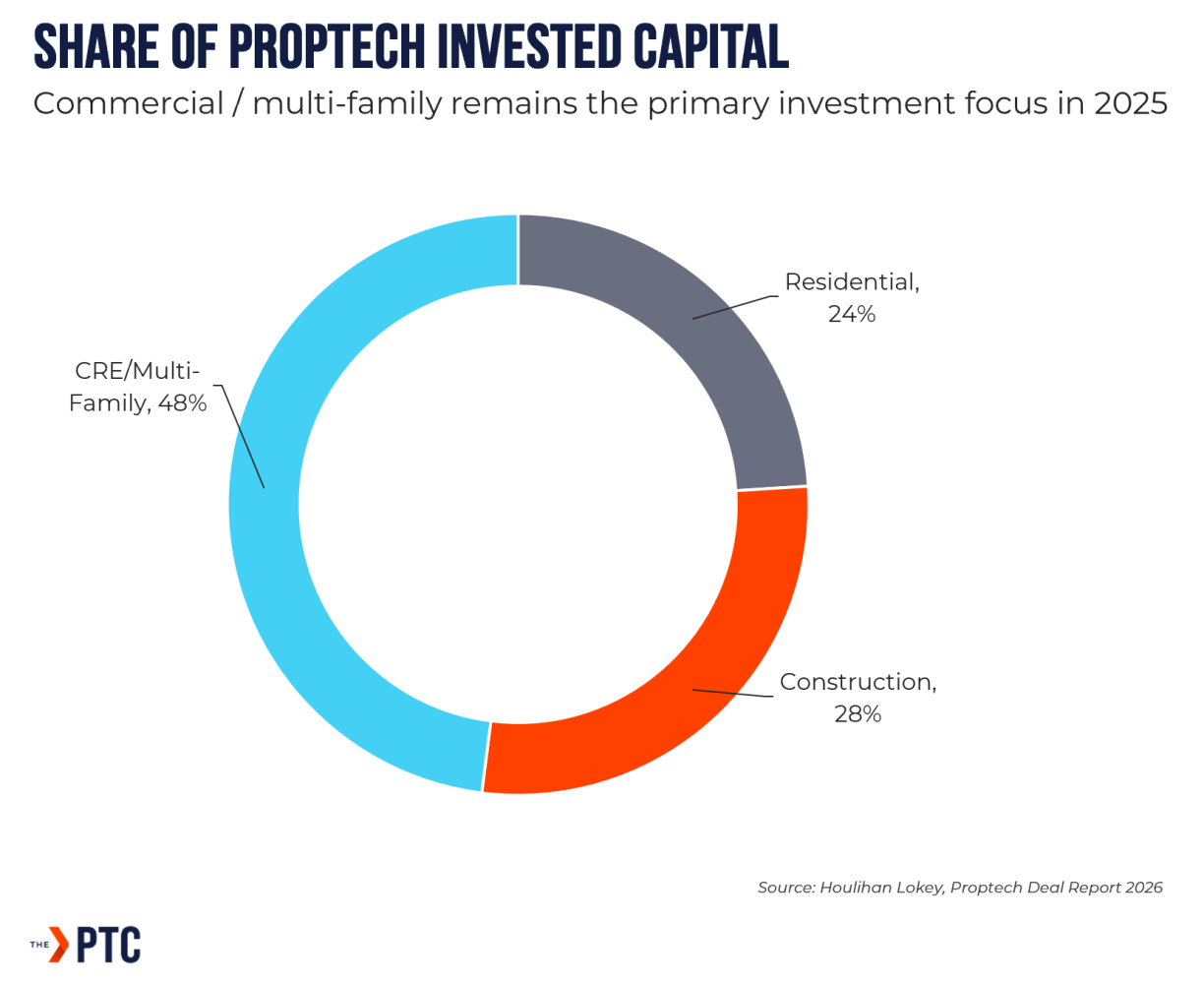

Investors' interest in Contech is real and growing. According to Holihan Lokey, the share of capital invested in Contech, as a percentage of all proptech investment, increased from 23% to 28%. This figure understates related investment or corporate activity in construction materials and supplies, which has accelerated based on increased specialist tech approaches.

An example of the latter is the illustrative 2026 acquisition of Top Build by QXO for $ 17 billion.

This strategic acquisition shows the desire to have products and offerings throughout the building lifecycle, blends traditional products with technical offerings and gives a framework to support emerging and complex projects, including infrastructure and data centre developments.

QXO is not alone in using acquisition to ramp up capabilities rather than slowly innovate. Holcim, one of the leading innovators in the space, has announced that they are seeking to acquire 15 businesses alone in 2026, covering key aspects including sustainable materials, building tech and waste offerings.

The leading software platforms in Contech are also on the acquisition trail as they seek to enhance their offerings beyond their core.

In the last 18 months, leading Proptech VC fund, Fifth Wall, notes some key transactions:

These purchases tie into the trend we noted earlier in the article, for technologies to be successful, they move beyond one narrow solution (project management for example).

This approach has also attracted other strategic purchasers with the large acquisition of Consigli, the Norwegian AI design tool, by US consulting firm AECOM at the end of 2025, for example.

These approaches mirror the supply chain angle above and reflect a desire to control the entire workflow of a construction project in one place.

Although VCs and institutional investors are still active in Contech, the growth of M&A is driven by strategic investors. European Investment Advisory firm Flatman has shown the proportion of deals driven by strategic investors jumped from 64% in 2024 to 69% in 2025. From the PTC’s viewpoint globally, this is consistent with investor sentiment in other core markets too.

What are the key drivers looking at the market in aggregate? We see 3-4 key trends which often overlap.

Investor sentiment on standalone products vs consolidated offerings: Investors (such as PE giants) are accelerating the trend as they attempt to roll up complementary offerings.

Contech has certainly reached a critical point in its maturity. The industry now expects, rather than hopes, for a digitised construction world.

This has translated into corporate activity as the market moves to consolidate across techs, the lifecycle of build and supply chains and product offerings.

We see M&A accelerating as large players and platforms move quickly to establish their positions. Arguably, Contech is catching up to other spaces, and the marriage of tech capability and direct impact on margins will create opportunities for strategic investors and the wider ecosystem.

.webp)

.jpeg)

.jpg)

.jpg)

.jpg)

.webp)

.jpg)

.jpeg)

.png)

.png)

.jpg)

.jpeg)

.jpeg)

.jpeg)

.jpg)

.jpg)

.png)

.jpg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpeg)

.jpg)

.jpeg)

.jpg)

.png)

.jpeg)

.jpg)

.jpeg)

.png)

.jpg)

.png)

.png)

.png)

.jpg)

.jpg)

.jpg)

.png)

.webp)

.png)

.jpg)

.jpg)

.jpg)

.jpg)

.png)

.jpg)

.jpeg)

.jpeg)

.png)

.png)

.png)

.jpeg)

.jpeg)

.png)